Luxembourg CCUS & CDR ecosystem - Facts & Figures

Last update: May 2026

39 actors, 66 projects, 1 ambition: decarbonising Luxembourg

This Facts & Figures report provides a structured and data-driven overview of the CCUS & CDR Mapping for Luxembourg. This mapping has been developed in collaboration with the Luxembourg Ministry of the Environment, Climate and Biodiversity (MECB), as part of a national task force dedicated to mapping and structuring the Carbon Capture, Utilisation and Storage (CCUS) and Carbon Dioxide Removal (CDR) ecosystem in Luxembourg.

The study covers 39 organisations and 66 R&D projects that form the backbone of the national CCUS & CDR ecosystem, spanning the complete value chain: source, capture, transport, storage, utilisation and monetisation.

CCUS and CDR: Definitions and key concepts

CCUS — Carbon Capture, Utilisation and Storage: A set of technologies that capture CO₂ emissions from industrial processes or energy production, and either reuse them in processes or products (utilisation) or store them permanently underground (storage).

CDR — Carbon Dioxide Removal: Approaches that actively remove CO₂ directly from the atmosphere and store it durably, either through natural processes (e.g. reforestation, soil carbon) or engineered solutions (e.g. direct air capture).

Ecosystem overview

The Luxembourg CCUS & CDR ecosystem brings together 39 actors across all six stages of the carbon value chain. Two complementary categories structure the ecosystem.

CCUS value chain actors — the decarbonisation players

21 actors have decarbonisation as a primary mission. CCUS or CDR activities are at the heart of their business model. They are directly positioned on one or more steps of the CCUS value chain — source, capture, transport, storage, utilisation or monetisation — and contribute operationally to the deployment of carbon management solutions.

Enablers — the ecosystem supporters

31 actors support CCUS deployment through technologies, engineering, equipment, digital tools or advisory services. They provide solutions deployed either directly at specific stages of the CCUS value chain or in a cross-cutting capacity across the broader ecosystem.

Figure 1: Numbers and categories of stakeholders shaping the Luxembourg CCUS & CDR ecosystem

Source of data: Luxinnovation (2026 Luxembourg CCUS & CDR Ecosystem Mapping) N.B.: Some entities can be included in more than one category where relevant.

These categories are not mutually exclusive. Among the 39 organisations identified in the mapping, 13 play a dual role, acting simultaneously as value chain actors and enablers. These organisations combine operational CO₂ management activities with the provision of technologies or services to other actors in the ecosystem.

In contrast, organisations classified solely as value chain actors are primarily engaged in performing CO₂ management activities along the value chain for their own operations, without being identified as solution providers to others. Enablers, for their part, may operate at specific stages of the value chain, but their role remains supportive, providing the capabilities that enable other organisations to implement CO₂ management solutions.

As a result, the ecosystem is composed of 39 unique organisations, with:

- 13 dual-role actors

- 8 organisations acting solely as Value Chain Actors

- 18 operating exclusively as Enablers

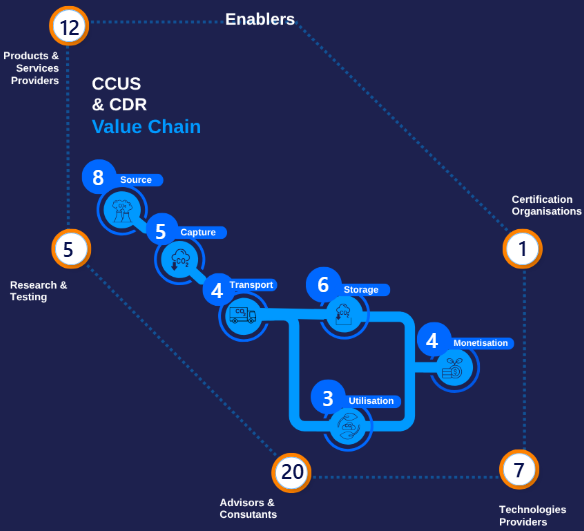

CCUS value chain overview

The CCUS value chain can be broken down into six segments, each with distinct roles and integration levels.

Figure 2: CCUS & CDR value chain

Source of data: Luxinnovation (2026 Luxembourg CCUS & CDR Ecosystem Mapping) N.B.: Some entities can be included in more than one category where relevant.

Enabler categories

Among enablers, advisors and consultants form the strongest cluster (present in over 60% of enabler classifications). This underscores how knowledge-based expertise is driving early market structure.

Technology providers and products & services providers create a practical backbone for implementation, while research & testing organisations anchor the innovation pipeline.

Figure 3: Distribution of entities by enabler category

Source of data: Luxinnovation (2026 Luxembourg CCUS & CDR Ecosystem Mapping) N.B.: Some entities can be included in more than one category where relevant.

Cross-analysis and strategic insights

Technologies and activities

The technology and activity trends described in this section reflect the ecosystem as a whole, covering both value chain actors and enablers. While these two groups share the same overarching goal, their profiles are markedly different.

Among value chain actors, technologies are more industrial in nature: BECCS, energy management and waste-to-energy dominate, with core activities centred on manufacturing and infrastructure provision. Capture and utilisation actors stand out with a stronger focus on R&D and solution development. Among enablers, consulting and service & solution sales are the primary activities, with a growing share moving toward training and solution development, signalling a gradual shift from strategy to action.

Across the ecosystem as a whole, data analytics, ESG consulting and energy management emerge as the most widely deployed technologies, reflecting a current phase dominated by knowledge-intensive activities rather than deep industrial deployment. On the abatement and removal side, circular economy practices, waste-to-energy and BECCS emerge as the main technological pathways. Finally, SaaS and cloud computing are taking shape in early development.

Figure 4: Top 10 key technologies by number of entities

Source of data: Luxinnovation (2026 Luxembourg CCUS & CDR Ecosystem Mapping) N.B.: Some entities can be included in more than one category where relevant.

Ecosystem maturity and size

Workforce and company size

Luxembourg’s CCUS & CDR ecosystem is clearly SME-driven, with a strong dominance of micro and small enterprises shaping the landscape. While a limited number of mid-sized players are beginning to bring more structure, large companies remain scarce and complete the landscape by providing structural depth to the ecosystem.

Figure 5: Workforce distribution of ecosystem actors

Source of data: Luxinnovation (2026 Luxembourg CCUS & CDR Ecosystem Mapping)

Ecosystem age and maturity profile

From an age perspective, the ecosystem shows a mixed but dynamic maturity profile.

Figure 6: Age distribution of ecosystem actors (since founding year)

Source of data: Luxinnovation (2026 Luxembourg CCUS & CDR Ecosystem Mapping) *No data available for 2 companies.

Luxembourg’s CCUS & CDR ecosystem shows a good balance between new and established actors. A large share of recent companies reflects the current momentum in climate tech, while a similarly important group is already moving into more advanced development phases. At the same time, a solid base of older, well-established players provides stability.

Overall, the trend points to a growing ecosystem that is expanding while gradually structuring itself, with both innovation and experience playing key roles.

Together, this distribution highlights an ecosystem where new entrants and long-standing actors coexist, signalling both early-stage momentum and a solid institutional backbone. The ecosystem remains characterised by a still-limited number of actors (39), a dominance of SMEs and micro-enterprises, and a research base not yet fully translated into commercial deployments, but one that is rapidly professionalising and gaining industrial traction.

R&D project insights

The Luxembourg CCUS & CDR ecosystem includes 66 active or completed R&D projects. Most are led by research associations (16), public institutions (16) and consortia (7), confirming the strong academic and public-sector foundation of Luxembourg’s innovation landscape. Over 80% of these initiatives are research-driven, with the remainder focused on consulting, engineering and prototyping.

Figure 7: R&D project focus areas across the CCUS value chain

Source of data: Luxinnovation (2026 Luxembourg CCUS & CDR Ecosystem Mapping)